The FIRE Movement is gaining momentum, and stories are emerging of people retiring as early as in their mid-30s. Even Alto’s own research showed that on average, millennials hoped to retire at age 59, well before the traditional retirement age and certainly younger than previous generations hoped for.

With all the enthusiasm surrounding the prospect of early retirement, it’s no wonder many are asking themselves, “Is retiring early really attainable? And how can I?”

Today, we’ll dive into what the FIRE Movement is, the pros and cons of early retirement, and three mistakes to avoid if you want to retire early.

What is the FIRE movement?

You may have heard the catchy acronym, but what exactly does it mean and what are the key principles? FIRE stands for Financial Independence, Retire Early. The term was coined by Vicki Robin and Joe Dominguez in their 1992 book, Your Money or Your Life, which included a nine-step program designed for those seeking to transform their relationship with money and ultimately retire early.

Followers of the FIRE Movement dedicate the majority of their income (usually around 70%) to savings and investments so they can retire much earlier than the conventional age of 65, with some even retiring as early as their 30s. The goal is to live frugally, save and invest aggressively, retire early, and live off their portfolio for decades before the conventional retirement age. While this path may seem appealing, it may not be for everyone, and there are pros and cons to early retirement.

The pros and cons of early retirement

Early retirement may sound dreamy, but there’s a lot to consider, and failing to plan could mean running out of money before you die. Still, it’s easy to imagine the pros of retiring early.

Pros of early retirement

According to U.S. News & World Report, the pros of early retirement include:

- Freedom from office constraints

- Time to pursue passions

- An improvement in well-being

- The opportunity to choose meaningful part-time work

- The ability to sit at the beach 24/7 (Okay, we added this one.)

Cons of early retirement

The cons of early retirement include:

- Years of no income

- Potential health insurance issues

- Feelings of loneliness

- Loss of purpose

Life expectancy after retirement

While there are certainly many factors to consider, making sure you have enough money to live on post-retirement is crucial. Though life expectancy in the U.S. has dropped in the last two years due to COVID-related deaths, U.S. Census experts predict a six-year life expectancy increase by 2060, which could make a big difference for early retirees if not properly taken into consideration. The financial component will be our area of focus in this blog.

Avoid these 3 mistakes if you want to retire early

Here are some common mistakes to avoid if you want to retire early. While mistakes aren’t limited to these three, they’re some of the more common errors, especially because they’re rooted in long-held investment advice and human nature.

Mistake #1: following the 4% rule

William Bengen was the financial advisor who invented the 4% rule. Often called “The Bengen Rule,” the 4% rule is a formula used to determine the amount of money a retiree can spend each year in retirement. According to the rule, you can withdraw up to 4% of your portfolio’s value in the first year of retirement, adjusting for inflation in subsequent years.

As an example, if your portfolio was $1 million, you could withdraw $40,000 in the first year. If inflation were 2%, you could withdraw $40,800 ($40,000 x 1.02) the second year, and so on. Using historical data for stock and bond returns, Bengen found that most retirement portfolios would last for around 30 years (and some as many as 50 years) with this formula.

However, the problem with the 4% rule is that it was based on overly simplified assumptions and may not be optimal for those in the FIRE Movement who need to make their retirement stretch at least 50 years. These simplified assumptions include:

- Reliance on historical returns/data

- A 30-year retirement horizon

- Returns equal to those of market indexes

- Not accounting for fees

- A portfolio invested only in domestic assets

- A fixed percentage withdrawal (“dollar plus inflation”)

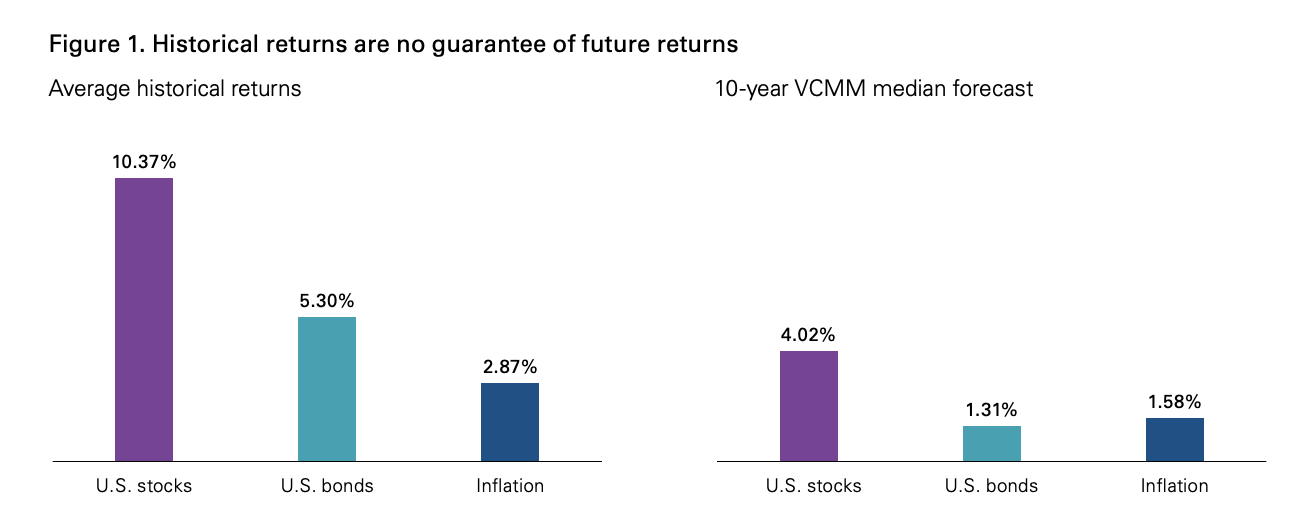

The graph below demonstrates that average historical returns for stocks and bonds may no longer be an accurate and reliable predictor of future returns. The 10-year Vanguard Capital Markets Model® (VCMM) median forecast predicts modest 4.02% returns for stocks and 1.31% returns for bonds. Do we even need to mention the fact that inflation is currently sitting at 8.3%?

Instead of following the “dollar plus inflation” withdrawal rule, many in the FIRE Movement are turning to dynamic spending models that account for actual market performance, rather than static spending rules.

The Yale University endowment is notorious for its positive performance and alternative asset allocation. It’s no wonder one of the most popular dynamic spending models is the Yale Spending Rule, which includes the following formula:

70% of the amount of the distribution from the previous year (adjusted for inflation) + 30% of the moving average of the endowment’s balance over the past three years multiplied by a set spending rate (e.g., 5%)

The benefits of choosing a dynamic spending model as opposed to the long-held 4% rule are that you can correct course based on the market’s performance, enjoy greater withdrawals during strong markets, and decrease withdrawals during poor market conditions to help ensure you don’t run out of money post-retirement.

Mistake #2: not diversifying your investments

As mentioned earlier, many forecasts predict modest returns for stocks and bonds. That’s why it’s important to diversify your investments, not only across asset classes but also across investment platforms.

Diversifying Across Asset Classes

While the Yale University endowment is just that-an endowment fund-many FIRE Movement followers are taking a page from their book. After all, they’ve pioneered not only a formula to balance withdrawals for current and future initiatives but also for their alternative asset allocation.

Alternative assets offer the potential for outsized returns and can reduce exposure to public market volatility. That’s why institutional investors and the ultra-wealthy allocate, in many cases, up to 50% of their investment funds to alternative assets.

Diversifying Across Investment Platforms

While brokerages like Robinhood, Acorns, E*Trade, and Coinbase are popular, especially for younger investors, understanding the short- and long-term tax implications is vital. Brokerage accounts allow investors to buy and sell stocks and securities freely with no cap on the amount they can invest. However, investors will pay taxes on interest, dividends, and capital gain income in the tax year they earn it, which can not only get expensive but also complicated come tax time.

Opening a traditional or Roth IRA is a wise move as earnings will grow tax-deferred or tax-free until you’re eligible to take distributions at age 591/2. This can be an especially wise move for those in the FIRE Movement who want to secure a long-term investment vehicle and help ensure they have something to fall back on in the future. Additionally, if your employer offers a 401(k) match, take advantage of that free money, and don’t forget to roll over your 401(k) funds when you change jobs.

Initiate a 401(k) Rollover

Roll over your old 401(k) to an Alto IRA or Alto CryptoIRA®. Plus, check out our recent blog about the 4 ways to contribute to an IRA.

Mistake #3: keeping up with the Joneses

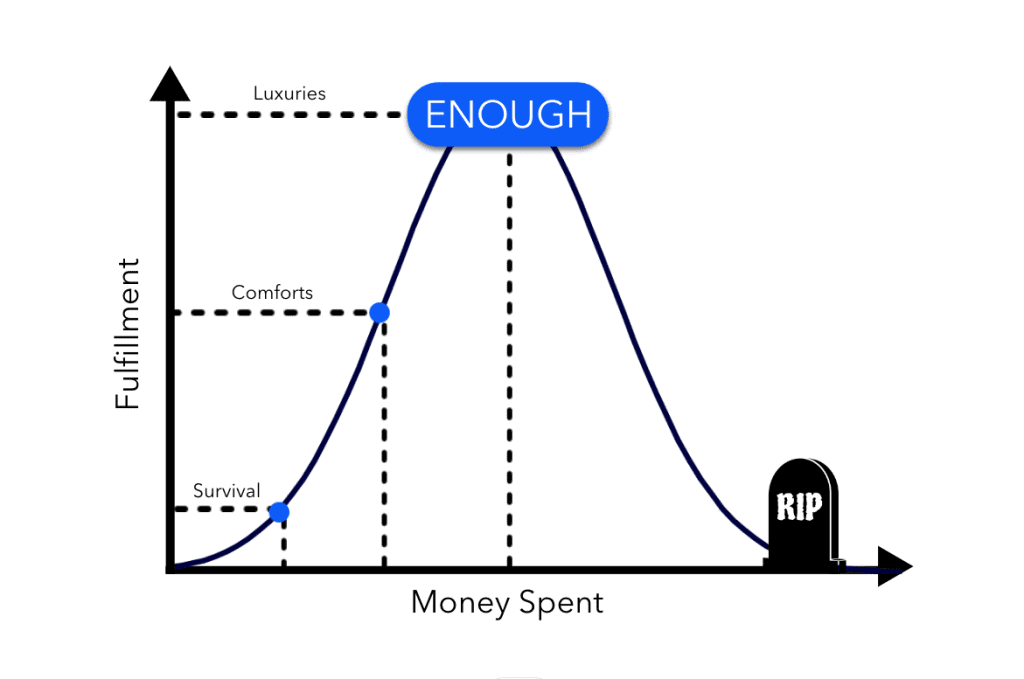

One of the key principles of the FIRE Movement is living within your means. As the movement’s founders so eloquently put in Your Money or Your Life, “You can never have enough if you are measuring by what others have or think. It’s like trying to go up on a down escalator. Other people’s opinions are fickle. Other people’s stuff is ever changing.”

The goal, as they go on to say, is at the fulfillment curve’s peak called “enough.”

Early retiree Steve Adcock, a self-made millionaire who retired at age 35, cited “ignoring the Joneses” as one of the reasons for his success, saying that focusing on his and his wife’s own goals helped them tune out the noise and ultimately accomplish what they set out to do.

Open a self-directed IRA with Alto

Just so we’re clear, we’re done with the cheeky “what not to do” phrases. Something you might consider, however, is opening an Alto IRA or CryptoIRA to diversify your investments beyond assets available in public markets. While conventional IRAs only allow limited investment opportunities, a self-directed IRA puts you in the driver’s seat when it comes to your investments. (Something FIRE Movement believers are all about.)

With an Alto IRA, you can invest in art, real estate, venture capital, and more. An Alto CryptoIRA enables you to invest in [acf field=”crypto_number” post_id=”options”] crypto assets through our integration with Coinbase, offering one of the largest coin selections of any crypto IRA.

Open an account today to get started.