While stocks and bonds have historically served as the core components of portfolio diversification, recent market shifts have prompted discussion about the effectiveness of this traditional mix under changing economic conditions.

A 60% equities and 40% bonds allocation has served as a foundational model for asset allocation. It offered a mix of growth and stability, and for many investors, it remained a reliable framework throughout various market cycles.

Over time, though, it’s become harder to overlook the signs. Market events have gradually shown that the old playbook may no longer be as effective as it once was.

In 2022, the 60/40 portfolio posted its worst year since the Great Depression1.

With a decline of approximately 16-18% in 2022, the 60/40 portfolio — long regarded as a core strategy for balanced investing — experienced one of its most challenging years in recent history, highlighting unexpected correlations between asset classes during periods of market stress.

When stocks zigged, bonds zigged too. What was once considered diversification revealed a higher level of correlation than many investors expected2.

The culprit isn't cyclical market volatility—it's structural change. Persistent inflation, supply chain disruptions, geopolitical realignments, and central bank policy shifts have fundamentally altered how assets interact3, revealing a harsh truth: this environment has underscored an important consideration: achieving effective diversification may require looking beyond traditional allocations of stocks and bonds.

Why Real Diversification Means Rethinking Asset Allocation

BlackRock CEO Larry Fink has noted that traditional portfolio models, such as the 60/40 split, may no longer offer the same diversification benefits they once did, particularly in the face of persistent inflation and correlated asset class behavior.

Where to next? Real diversification.

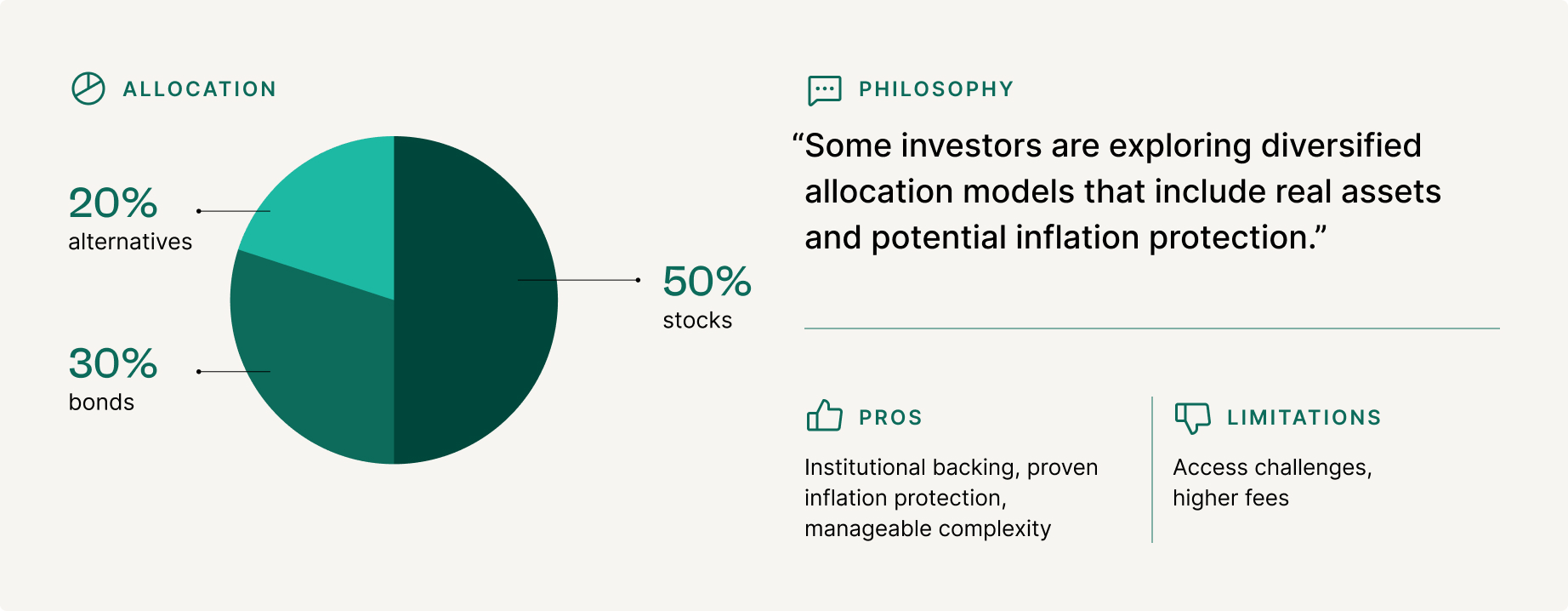

Larry Fink's 50/30/20

- Allocation: 50% stocks, 30% bonds, 20% alternatives

- Philosophy: "Some investors are exploring diversified allocation models that include real assets and potential inflation protection."

- Pros: Institutional backing, proven inflation protection, manageable complexity

- Limitations: Access challenges, higher fees

Larry Fink further explains that new models, such as the 50/30/20 framework, allocate 20% to private assets like real estate, infrastructure, and private credit.

Infrastructure investments offer two potential benefits: inflation protection through revenue streams that typically rise with inflation4 (think tolls and utility payments), and have historically exhibited lower return volatility than public markets.

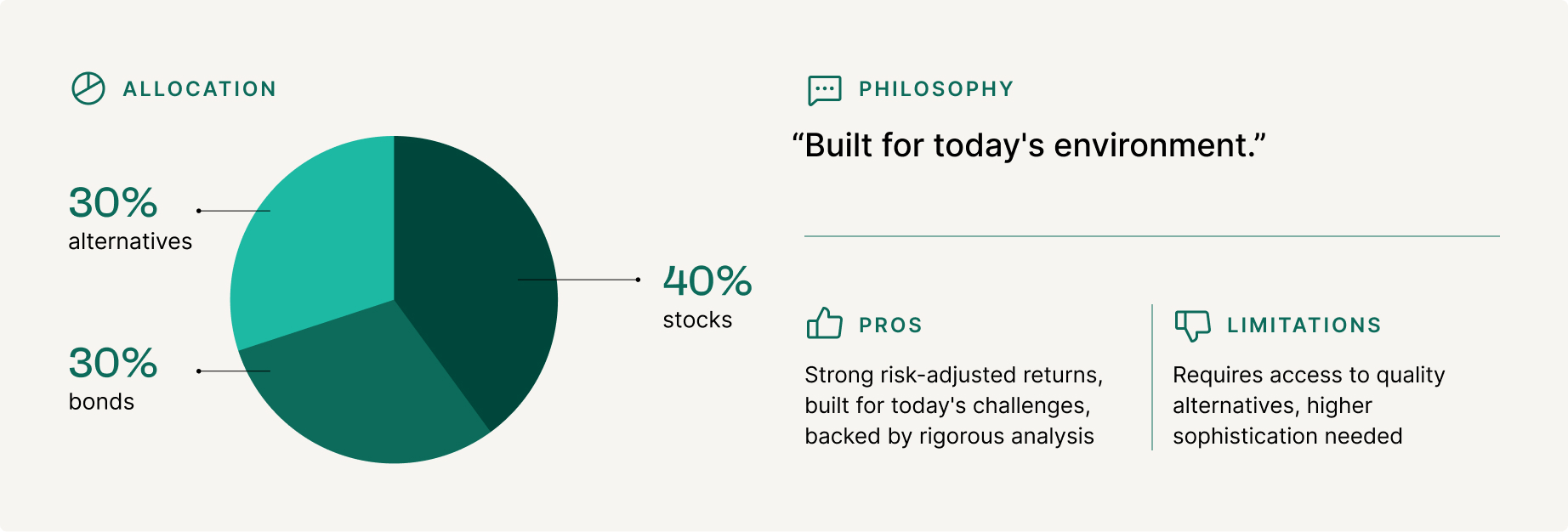

Fink's approach builds on decades of research from Markowitz's Modern Portfolio Theory, Fama and French's factor models, and Ray Dalio's "all-weather" concepts. The 20% alternatives allocation provides meaningful diversification without overwhelming complexity. However, such allocations also introduce unique risks, including illiquidity, valuation uncertainty, and higher fees, and may not be suitable for all investors.Kohlberg Kravis Roberts & Co. (KKR), a global investment firm known for its expertise in private equity, credit, and assets, regularly publishes macro insights and portfolio strategies. One notable framework they use is the 40/30/30 model, which re-examines traditional asset allocation.

KKR's 40/30/30

- Allocation: 40% stocks, 30% bonds, 30% alternatives

- Philosophy: "Built for today's environment"

- Pros: Strong risk-adjusted returns, built for today's challenges, backed by rigorous analysis

- Limitations: Requires access to quality alternatives, higher sophistication needed

KKR advocates for a 40/30/30 portfolio5 designed to reflect the current economic environment. Their research shows that this allocation outperformed traditional 60/40 by 2.6 percentage points between June 2020 and June 2022, with improved risk-adjusted returns6. These results are based on modeled returns using proprietary assumptions and are not indicative of future performance.

The 40/30/30 model is designed to introduce meaningful exposure to alternative investments while maintaining a level of liquidity that some investors may find appropriate. It reflects an asset allocation strategy developed in response to macroeconomic themes such as persistent inflation and supply chain disruption.

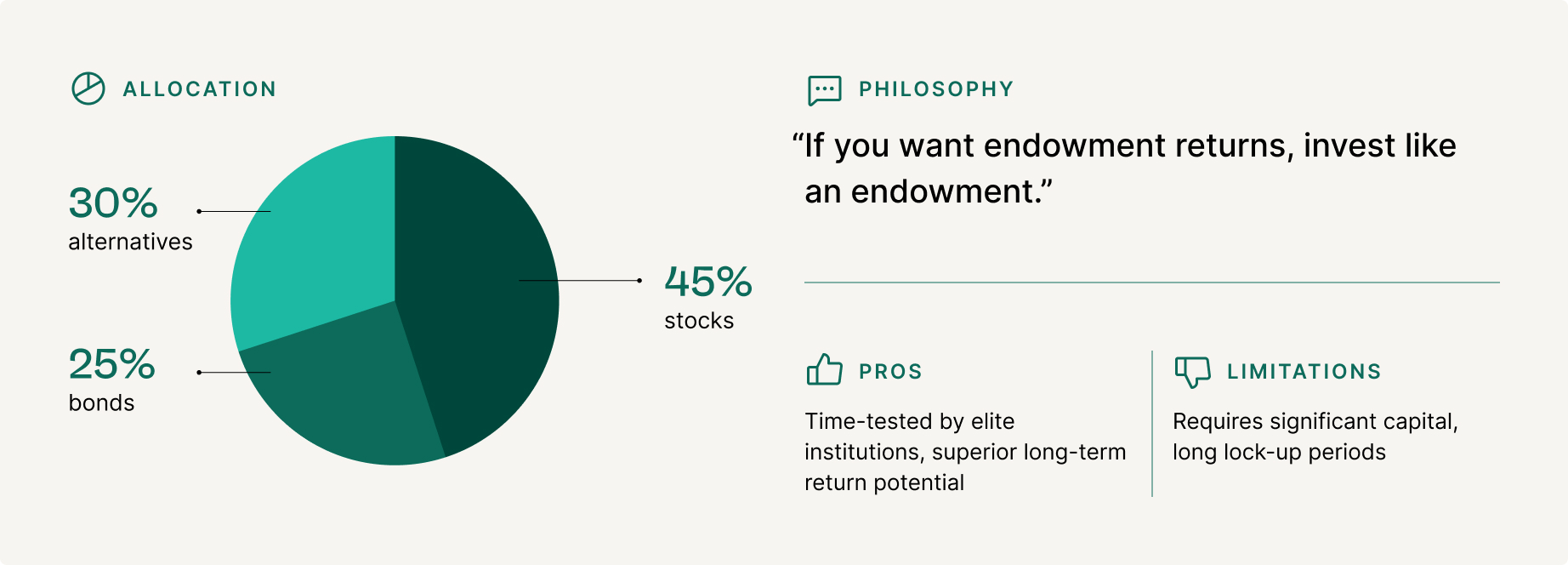

Finding Institutional Inspiration in the Yale Endowment Model

The Yale Model: 45/25/30

- Allocation: 45% stocks, 25% bonds, 30% alternatives

- Philosophy: "If you want endowment returns, invest like an “endowment"

- Pros: Designed to provide broad diversification across public and private markets

- Limitations: Requires significant capital, long lock-up periods

Some of the most aggressive asset allocation models are inspired by the approaches used by large institutional investors, including university endowments. For example, Yale's endowment has generated approximately 11.3% annual returns since the early 1990s, with significant alternatives exposure7.

This allocation reduces equity exposure while maintaining growth potential through alternatives that often outperform public markets over full cycles. It's for investors who prioritize long-term wealth creation over short-term liquidity. However, these investments are typically characterized by longer lock-up periods, complex structures, and limited liquidity, and may not be appropriate for all investors.

Access Was the First Hurdle for Individual Investors

The transition from 60/40 faces one critical obstacle: the right account structure. While institutions have used these strategies for decades, individual investors have been limited by traditional account restrictions.

When BlackRock's Larry Fink notes that "bridging the divide between the 50/30 and the 20 is almost impossible for most individuals," he’s referencing the challenges retail investors face in gaining meaningful exposure to alternative assets8.

Alto was built to help solve this problem. According to internal data, approximately 45% of Alto users allocate 10% or more of their portfolios to alternatives, compared to 18% of investors who do not use the platform. These figures reflect usage trends and are not predictive of investor outcomes.

Our platform enables investors to access specific alternative investment opportunities, such as direct private offerings, specialized real estate investment trusts (REITs), or alternative funds, that may be available to qualified self-directed individual retirement account (SDIRA) holders. While some of these investments have historically been more common among institutional investors like endowments and family offices, availability, terms, and access may vary based on eligibility, offering structure, and investor qualifications. The power of building these allocations within a tax-advantaged SDIRA cannot be overstated. Roth SDIRAs offer tax-free growth on alternatives, while Traditional SDIRAs provide tax-deferred growth—both allowing for more investment types than traditional IRAs. With over 26,000 investors and $1.2 billion in assets under custody, Alto has become the trusted bridge between individual investors and institutional-quality alternatives.

Access Is No Longer the Problem — Timing Is

The traditional 60/40 portfolio remains widely used, but a growing number of investors and institutions are evaluating alternative approaches in response to evolving market dynamics. While views differ on the pace and degree of portfolio adjustments, some have begun reallocating toward models that include a broader mix of asset classes, including alternatives.

Whether you're drawn to Larry Fink's measured 50/30/20 approach, KKR's optimized 40/30/30 framework, or the Yale-style 45/25/30 strategy, it starts with access. Use your Alto IRA and begin exploring opportunities to use a tax-advantaged account to invest in alternatives, including private markets and crypto. The institutions have already started the transition. The research supports the change. The access exists.

The only variable left is timing, and in investing, timing often favors those who act on conviction rather than those that wait for consensus.