As investors increasingly look to diversify their retirement portfolios with alternative assets like cryptocurrency, self-directed IRAs (SDIRAs) have gained attention as a flexible account option.

Unlike a traditional retirement account that is often limited to stocks and mutual funds, a self-directed IRA offers greater flexibility. However, this flexibility comes with a range of fees that can vary widely between providers. For investors considering crypto in 2025, a thorough SDIRA fees comparison is a critical first step toward making a smart investment decision.

Understanding self-directed IRAs and their role in crypto investing

A self-directed IRA is a retirement account that allows account owners to hold a broader range of investment options than traditional IRAs. This includes alternative investments such as:

- Real estate

- Precious metals

- Private equity

- Cryptocurrencies

The structure provides greater control over investment decisions, enabling a more diversified retirement portfolio.

The table below compares traditional IRAs and self-directed IRAs to highlight their key differences, especially in the context of crypto investing:

Their appeal for crypto investing stems from this flexibility. Self-directed IRAs provide a tax-advantaged way to invest in digital assets, which are not typically available through standard brokerage firms.

Understanding the different types of accounts and their rules is crucial for leveraging these tax benefits effectively. This guide will explore what sets these accounts apart and the crypto assets they can hold.

What sets self-directed IRAs apart from traditional retirement accounts

The primary difference between a self-directed IRA and a traditional IRA or Roth IRA lies in the scope of investment options. Traditional accounts offered by major brokerage firms like Charles Schwab typically restrict investors to traditional assets such as stocks, bonds, and mutual funds. In contrast, a self-directed IRA empowers account owners to invest in a wide array of alternative assets, including real estate, private equity, and precious metals.

This expanded freedom comes with greater responsibility. While a traditional IRA custodian often manages asset selection, self-directed IRA custodians, such as the Entrust Group or Equity Trust, primarily handle administration and ensure compliance. The account owner is responsible for all investment decisions, due diligence and navigating the fee schedule, which can include a setup fee, annual fee and administrative costs.

For experienced retirement savers who want hands-on control and access to unique investment opportunities, self-directed IRAs can be a great fit. It allows them to build a portfolio tailored to their specific knowledge and goals, all while retaining the same tax benefits and contribution limits as other types of accounts.

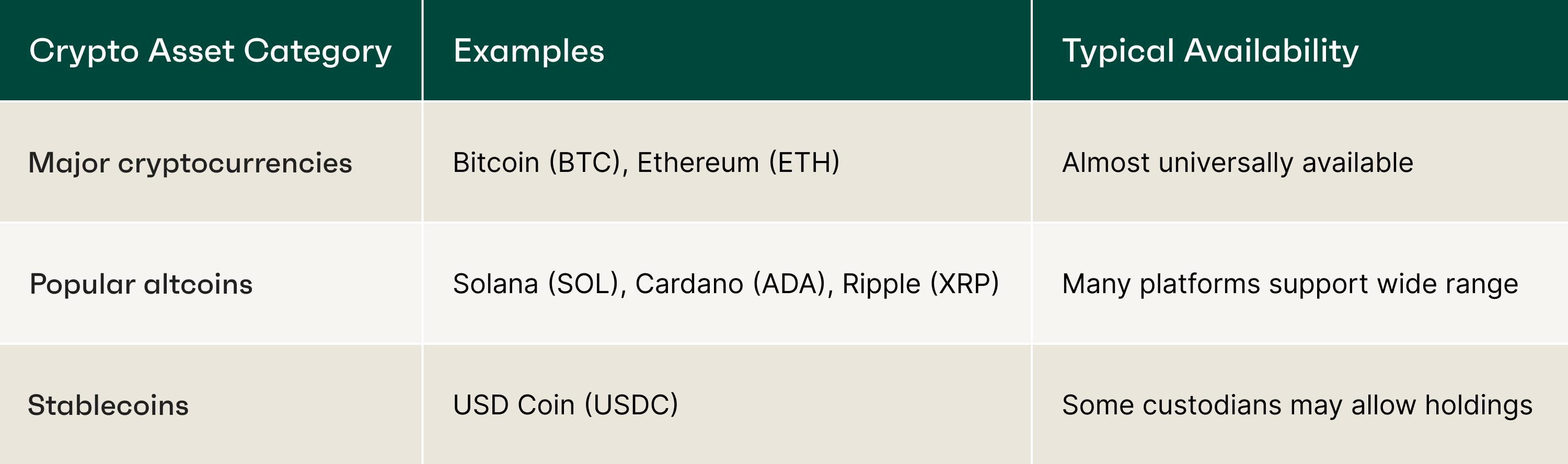

Crypto asset options within self-directed IRAs

Cryptocurrency can be a compelling alternative investment option available through a self-directed IRA. Unlike a standard retirement account, a crypto SDIRA allows investors to hold digital assets directly, offering a way to diversify beyond asset types like real estate or private equity. The range of supported crypto assets can vary significantly depending on the self-directed IRA provider.

Leading platforms have expanded their offerings to meet growing demand. For example, the Alto CryptoIRA® provides access to over 250 cryptocurrencies through its integration with Coinbase. Other providers like iTrustCapital and Rocket Dollar also support a variety of digital currencies. This gives investors the flexibility to make investment decisions based on their research and risk tolerance.

Key SDIRA providers for crypto investments in 2025

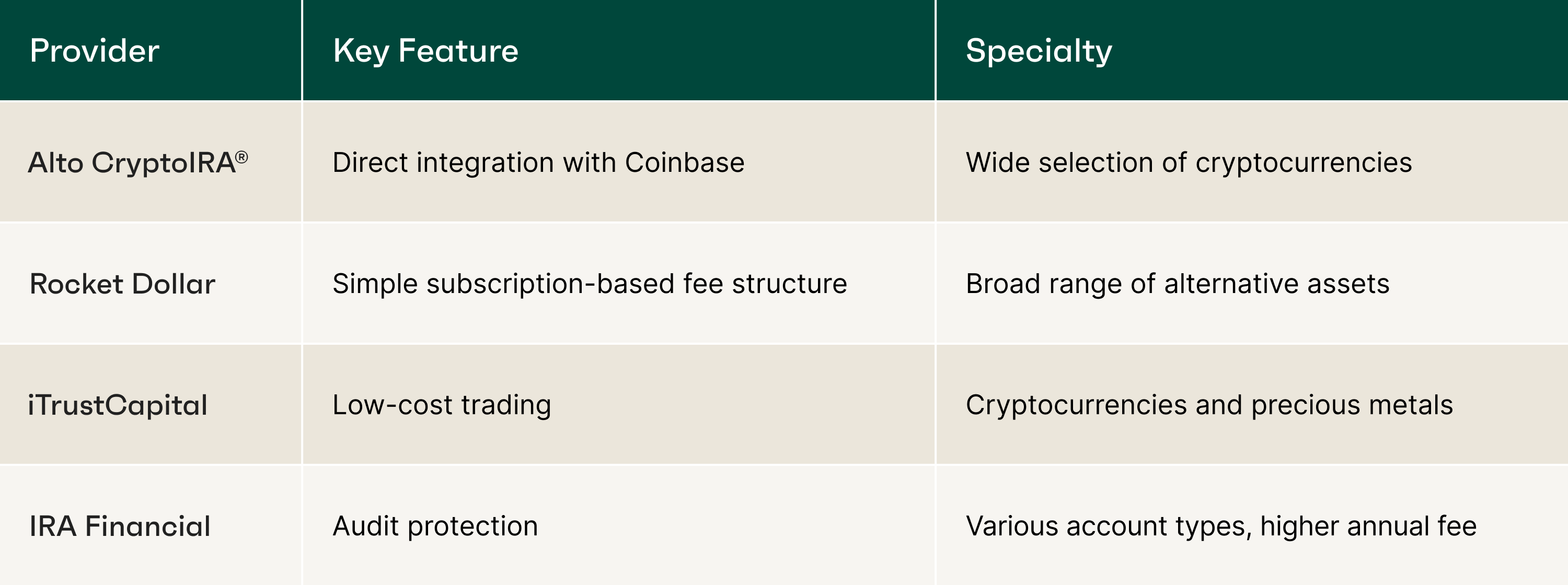

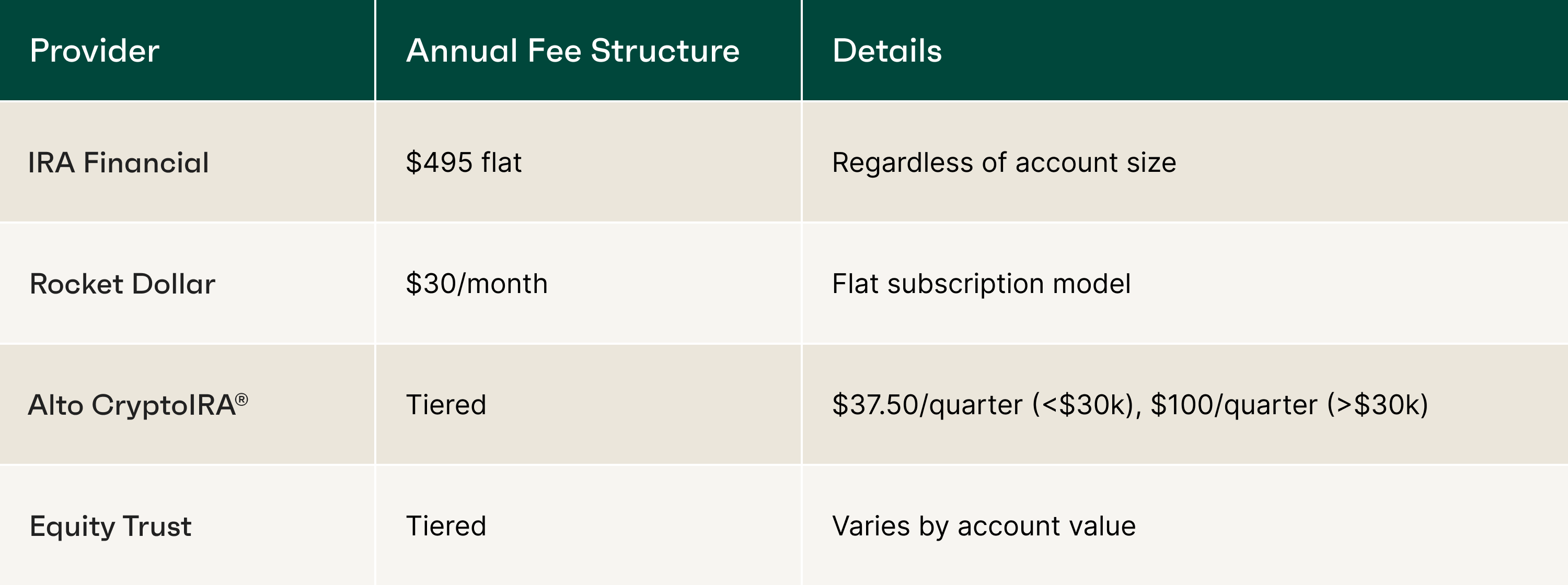

In 2025, a growing number of self-directed IRA custodians cater specifically to crypto investors. Prominent names in the space include Alto CryptoIRA®, Rocket Dollar, iTrustCapital and IRA Financial. Each of these providers offers unique features and a distinct fee structure, making it essential for investors to compare them carefully before committing.

When evaluating these self-directed IRA custodians, key criteria to consider are:

- The types of cryptocurrencies offered

- The security of the storage solution

- The complete fee schedule

Understanding these differences will help investors find a platform that aligns with their financial goals and investment strategy. Let's look at an overview of these major players and their notable features.

Overview of major custodians offering crypto-focused SDIRAs

Several self-directed IRA custodians have emerged as leaders in the crypto space, each with a different approach. These platforms are designed for account owners who want to move beyond traditional brokerage firms and add alternative investments to their retirement portfolios. While they all offer tax benefits, their services and fee schedules differ.

These custodians aim to simplify the process of holding alternative assets. Unlike traditional financial institutions, they do not offer investment advice; the responsibility for all investment decisions rests with the account owner. Understanding their unique offerings helps investors select the best platform for their needs.

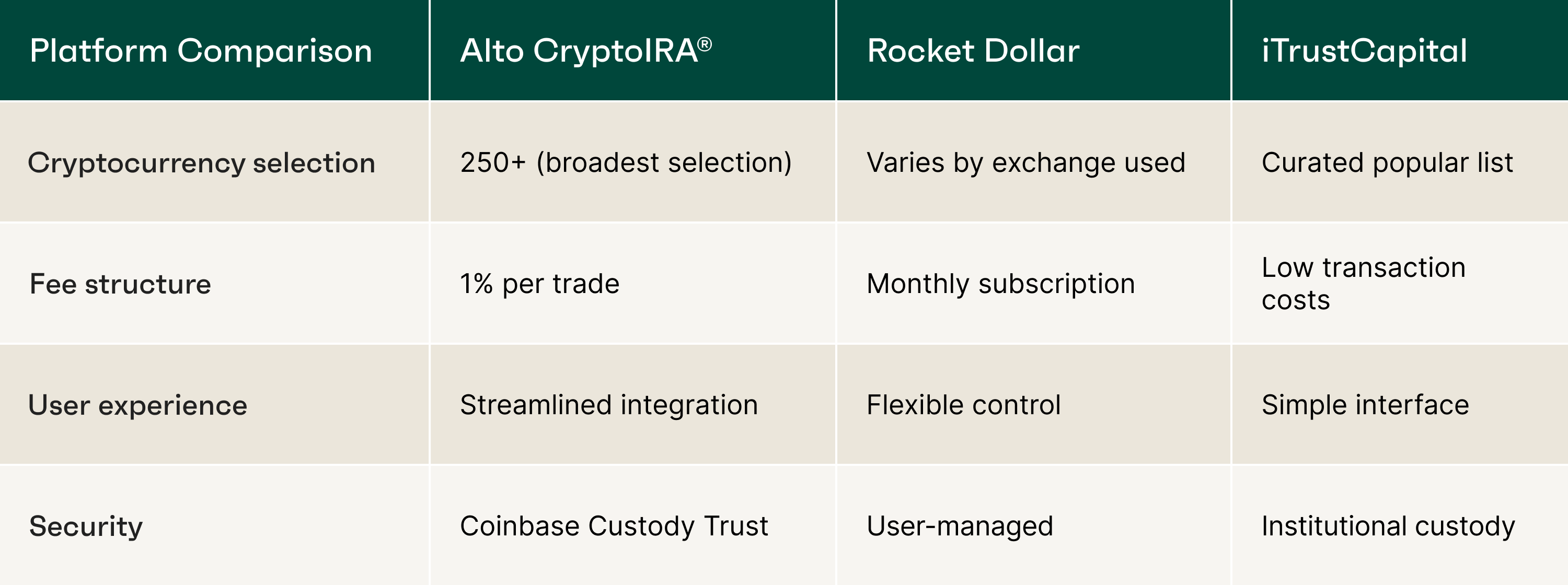

Notable features of Alto CryptoIRA® and comparable platforms

The Alto CryptoIRA® stands out due to its seamless integration with Coinbase, one of the world's largest cryptocurrency exchanges. This partnership gives account owners access to over 250 digital currencies, providing extensive diversification opportunities within a single SDIRA account. The fee structure is transparent, featuring a 1% trade fee with no hidden custodial fees or high minimums.

When comparing Alto CryptoIRA® to other platforms, investors will notice different models. For instance, Rocket Dollar uses a subscription model with a one-time setup fee and a flat monthly charge. iTrustCapital, on the other hand, focuses on low transaction costs for a curated list of popular cryptocurrencies.

Comparing typical fee structures across leading self-directed IRA custodians

Typical fee structures among leading self-directed IRA custodians vary significantly, impacting profit margins for account owners. Generally, these custodians impose:

- Setup fees

- Annual fees

- Transaction fees, which can add up over time

For instance, some firms, like Equity Trust and Rocket Dollar, charge administrative costs that scale with account value, whereas others prioritize transparency with straightforward fee schedules.

Understanding the nuances of self-directed IRA custodial fees—whether for precious metals or alternative assets—enables investors to make informed decisions about their retirement portfolios. Note: Always consult a tax advisor or financial professional before making IRA investment decisions.

Setup and account opening fees explained

A setup fee is a one-time charge that some self-directed custodians levy to open a new account. This fee covers the initial administrative costs required to establish the self-directed IRA, whether it is a Traditional IRA, Roth IRA or another account type.

Not all providers charge this fee, which makes it an important point of comparison for new investors.

When evaluating self-directed custodians, account owners should consider the setup fee in the context of the overall fee structure. A provider with no setup fee might have a higher annual fee or transaction costs, so it is crucial to look at the complete picture before making investment decisions.

Annual account maintenance charges

The annual fee, also known as an account maintenance fee, is a recurring charge for the ongoing administration of a self-directed IRA. These administrative costs cover services like record-keeping, reporting and ensuring compliance. The structure of this fee varies widely among SDIRA custodians and can be a flat rate or based on the total account value.

For account owners, the choice between a flat or asset-based annual fee depends on their current and projected account value. A flat fee may be more cost-effective for larger accounts, while an asset-based fee might be preferable for those just starting to build their self-directed IRA.

Transaction and trading fees for cryptocurrencies

Transaction fees, or trading fees, are charges incurred each time an investor buys or sells an asset within their self-directed IRA.

For crypto IRA investors, these fees are particularly important as they can accumulate quickly, especially for active traders. The way these fees are calculated differs significantly among self-directed IRA custodians.

When comparing crypto IRA fees, it is crucial to understand this distinction. A platform with integrated trading may offer convenience and clarity, while a checkbook IRA provides more flexibility but requires the investor to manage external exchange fees. The right choice depends on the investor's trading frequency and preference for an all-in-one solution versus greater control.

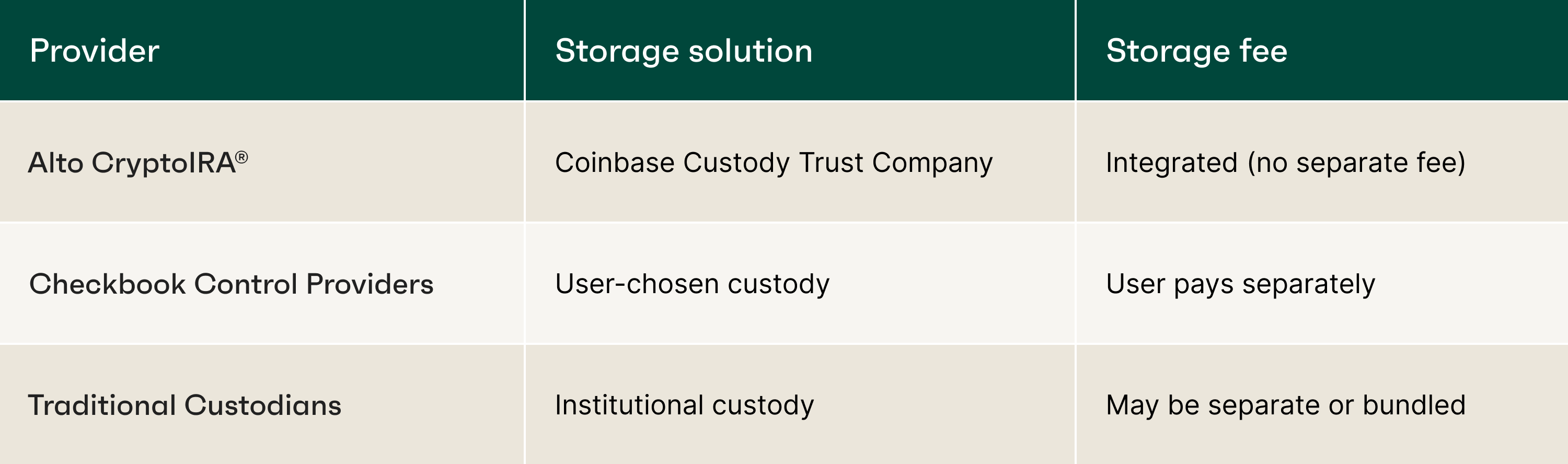

Storage and custody costs for digital assets

Storing digital assets securely is a critical function of a crypto SDIRA, and it often comes with associated costs. These storage and custodial fees cover the safeguarding of cryptocurrencies, which are typically held in institutional-grade cold storage to protect them from theft and hacking.

These costs can be bundled into the annual fee or charged separately.

Providers like Alto CryptoIRA® simplify this for investors. The crypto storage is managed by a qualified custodian, Coinbase Custody Trust Company, and the costs are integrated into its overall fee structure, so there is no separate storage fee. This offers peace of mind and predictability. In contrast, SDIRA custodians offering ‘checkbook control’ place the responsibility of choosing and paying for a secure wallet or custody solution directly on the account owner.

When analyzing the fee structure of an SDIRA, investors should clarify how digital assets are stored and what, if any, separate custodial fees apply. A provider that includes secure storage without an extra charge offers significant value and reduces the administrative burden on the investor.

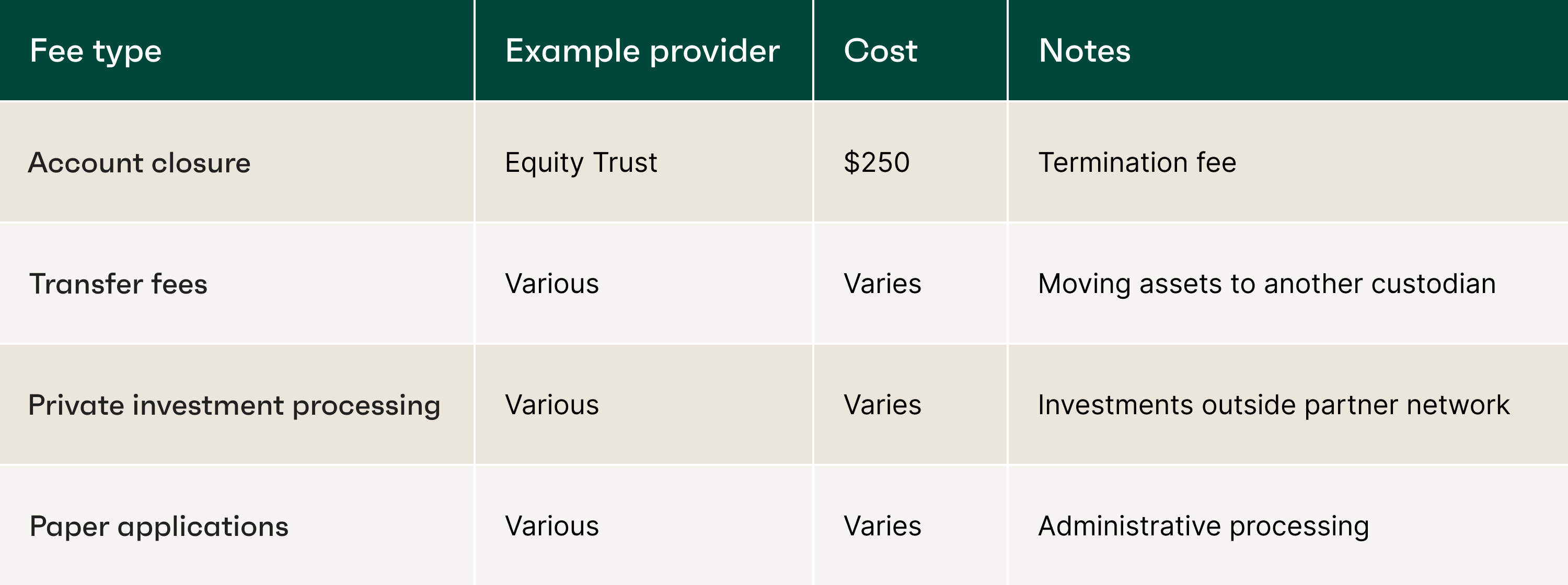

Hidden costs and investor considerations

Beyond the standard setup, annual and transaction fees, investors must be aware of potential hidden costs. These less obvious charges, such as a transfer fee or account closure fee, can come as an unwelcome surprise and affect the net returns on a retirement portfolio. Understanding the full fee schedule is part of the necessary due diligence for any self-directed IRA.

These costs are particularly relevant for alternative investments like crypto, where unique circumstances can trigger additional charges. By identifying these potential expenses in advance, account owners can better plan their long-term investment strategy and avoid fees that could diminish their tax-advantaged growth. The following sections will shed light on these uncommon charges and crypto-specific costs.

Uncommon charges: Transfer, closure and miscellaneous fees

While not always prominent in marketing materials, miscellaneous fees can play a significant role in the total cost of a self-directed IRA. These charges often relate to administrative actions outside of regular account maintenance.

Common examples include:

- An account closure fee, charged when an investor decides to terminate their account

- A transfer fee for moving assets to another custodian

Before opening an account, investors should carefully review the entire fee schedule provided by the self-directed custodian. Asking direct questions about fees for account closure, asset transfers and other non-standard transactions is a crucial step. This ensures full transparency and helps avoid unexpected charges down the road.

Crypto-specific costs and exceptions investors may encounter

Investing in crypto through a self-directed IRA can introduce costs that are unique to digital assets. These crypto-specific fees go beyond standard transaction and annual fees and can catch unprepared investors by surprise. Understanding them is vital for accurately projecting the performance of a retirement portfolio.

For instance, investors using a checkbook control IRA may be responsible for network fees (or "gas fees") when moving crypto between wallets. Some platforms may also have different fee tiers for trading certain types of alternative assets or charge extra for specialized custody solutions required for less common tokens.

Key takeaways for crypto IRA investors

By comparing the various costs related to account setup, annual maintenance and transactions, investors can make informed decisions that align with their financial goals. Additionally, being aware of hidden charges and crypto-specific fees will help mitigate any surprises along the way.