Insights from Alto’s educational series with Long Angle’s investment team

This content is intended for educational and informational purposes only and was produced without financial compensation.

Private markets have moved from the margins of portfolio conversations to the center.

As traditional public market frameworks face new pressures, investors are asking more nuanced questions. Some are seeking clarity on what private markets encompass and how they can be accessed. Others are focused on evaluating managers, assessing risk, and constructing portfolios with greater precision.

A desire to help bridge that gap is what motivated the launch of our three-part educational series, Investing Beyond the Traditional Playbook, produced in partnership with Long Angle’s investment team.

Private market investing calls for a deeper understanding of investment structures, rules and risks. Fund structures differ from traditional public securities, liquidity timelines extend over years rather than days, and performance outcomes can vary meaningfully depending on manager selection and strategy. Approaching this space thoughtfully requires understanding both the underlying investments and how those exposures function within a broader portfolio.

Throughout the series, we examined the structural shifts shaping capital markets and shared practical frameworks investors can use to approach private markets with greater discipline and clarity. Below are five key themes that emerged, and what they mean for investors.

Investments in private markets involve a high degree of risk and are not suitable for all investors. These investments are typically illiquid, may have limited or no secondary market. Performance outcomes can vary significantly, and investors may lose some or all of their invested capital.

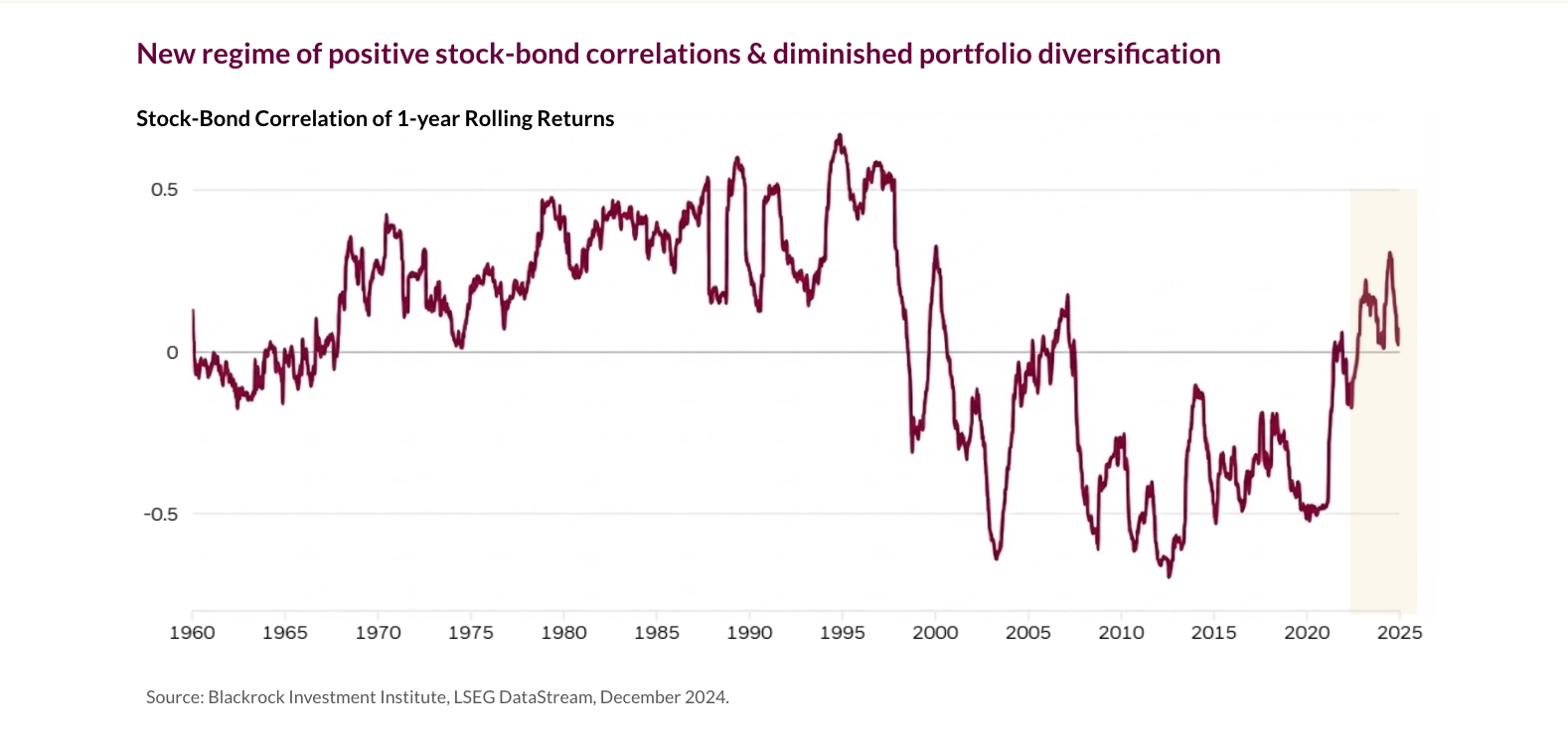

1. The traditional 60/40 portfolio is facing headwinds

For decades, the 60/40 portfolio has offered a straightforward formula: equities for growth and bonds for income and diversification.Today, that framework is being reassessed.

Blended earnings and coupon yields for a traditional 60/40 portfolio sit near historic lows, suggesting forward returns may be below long-term averages. At the same time, the negative correlation between stocks and bonds that supported diversification for much of the past three decades has weakened in a more inflationary environment.

The assumptions that drove strong risk-adjusted returns in prior decades are less dependable. Equity valuations remain elevated relative to history, bond markets have only recently reset after years of suppressed yields, and inflation has introduced more volatility across both asset classes.

In response, many investors are broadening the range of return drivers within their portfolios. Private markets are increasingly part of that discussion, offering exposure to different income streams, capital structures, and value creation dynamics that sit outside traditional public indices.

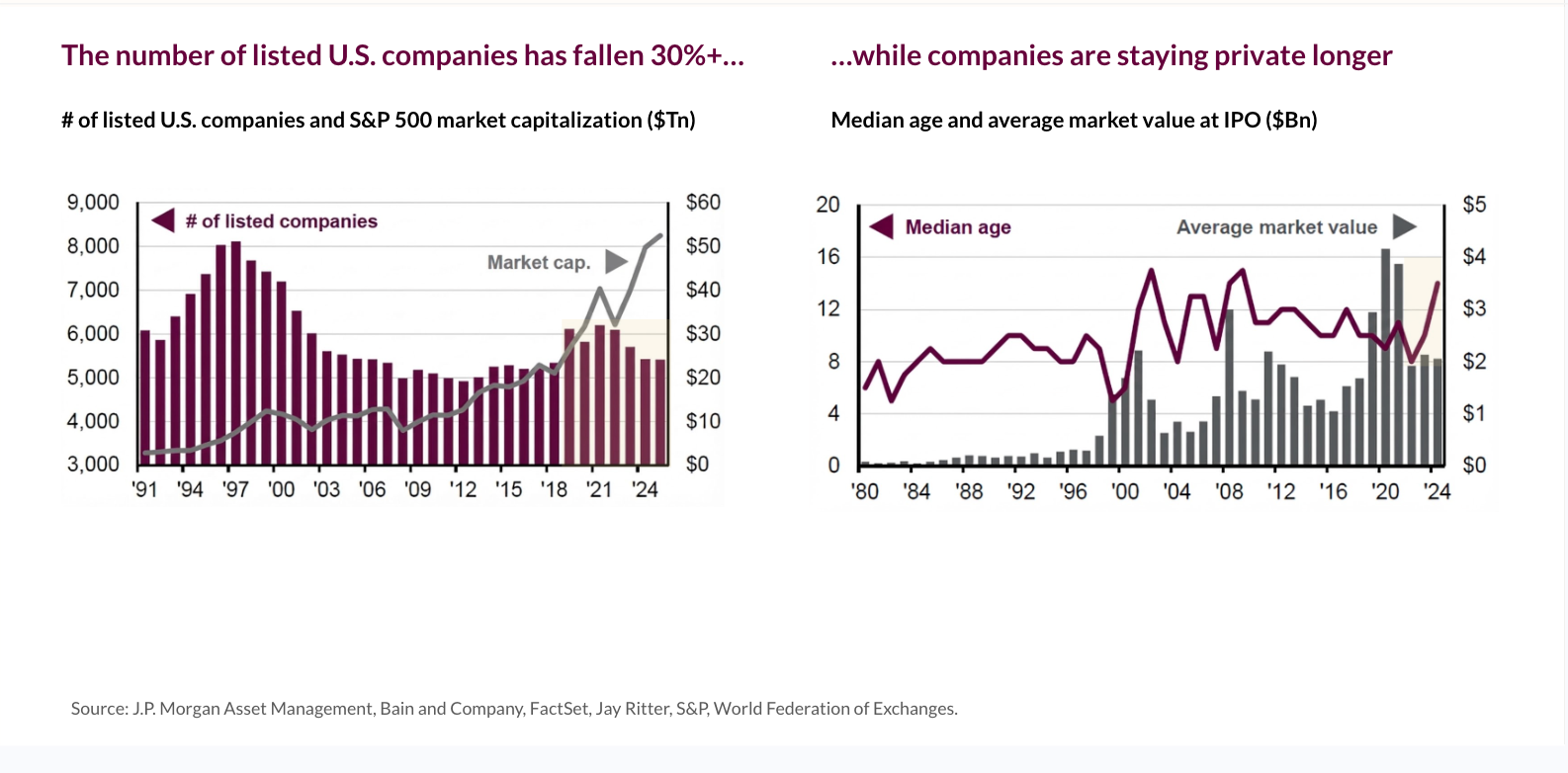

2. Public equity diversification is getting harder

The number of publicly listed US companies has declined meaningfully from its late 1990s peak even as total market capitalization has expanded. At the same time, a small group of mega-cap technology companies now represents a significant share of major indices, with the largest seven, often referred to as the “Magnificent 7,” accounting for more than 30 percent of the S&P 500. Earnings revisions have followed a similar pattern, with recent upward adjustments driven primarily by that narrow cohort while much of the broader index has seen downward revisions.

As a result, portfolios that appear diversified across hundreds of holdings are increasingly dependent on a handful of companies and a single dominant theme.

Private markets expand the investable universe. Today, most scaled US businesses with more than 100 million dollars in revenue are private, and are remaining private longer. A meaningful portion of value creation now occurs before a public listing. For allocators, that shift influences where and how growth exposure is sourced.

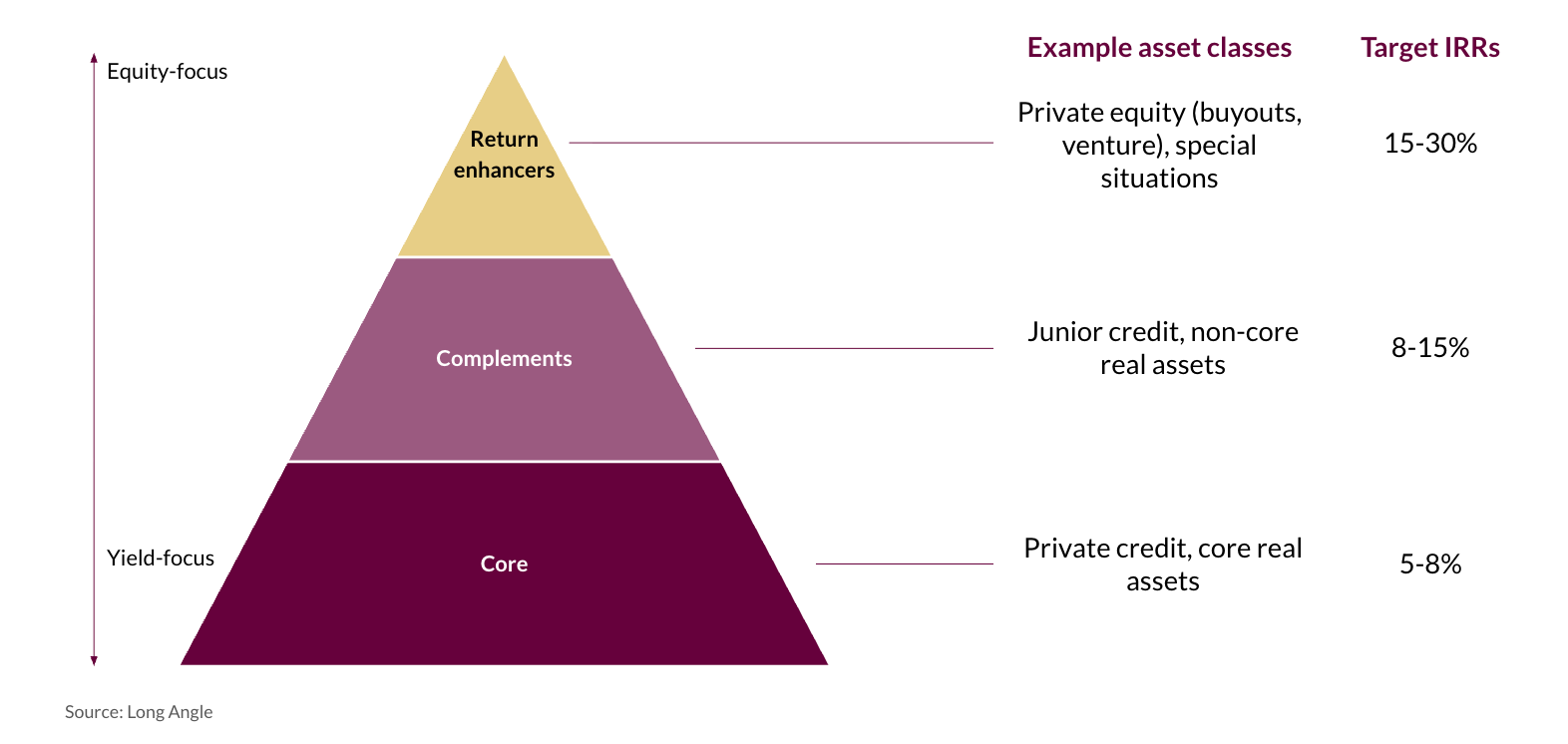

3. Private markets are strategy-driven

Private markets encompass a broad spectrum of strategies, each with distinct structures, risk profiles and return characteristics.

Private credit, buyout equity, venture capital, infrastructure, and real assets sit in different parts of the capital stack and generate returns in different ways. Some strategies emphasize contractual income and downside protection. Others rely on operational improvement, financial structuring or long-term growth to create equity value. Liquidity timelines, volatility expectations and outcome dispersion vary meaningfully across these categories.

Evaluating private markets through a single allocation lens can obscure those differences. A more constructive approach considers portfolio function: Where is income generated through cash flows? Where is operational execution driving margin expansion? Where is early-stage innovation creating asymmetric upside? Where does inflation sensitivity or sourcing advantage provide an incremental edge?

During the webinar series, Long Angle’s Min Park discussed a framework that organizes private strategies by their role within a portfolio. Income-oriented exposures such as private credit and core real assets may provide stability and predictable yield. Complementary strategies have historically targeted mid-teens returns with moderate risk. Equity-focused strategies, including buyouts and venture capital, pursue higher return potential alongside greater variability in outcomes.

Private credit illustrates how structural shifts create differentiated opportunities. As traditional banks have retrenched from middle market lending, private lenders have expanded to fill that gap. Many of these instruments are floating rate, influencing how they behave in changing interest rate environments and how they interact with traditional fixed-income allocations.

Clarity around which return driver is being accessed supports more deliberate portfolio construction.

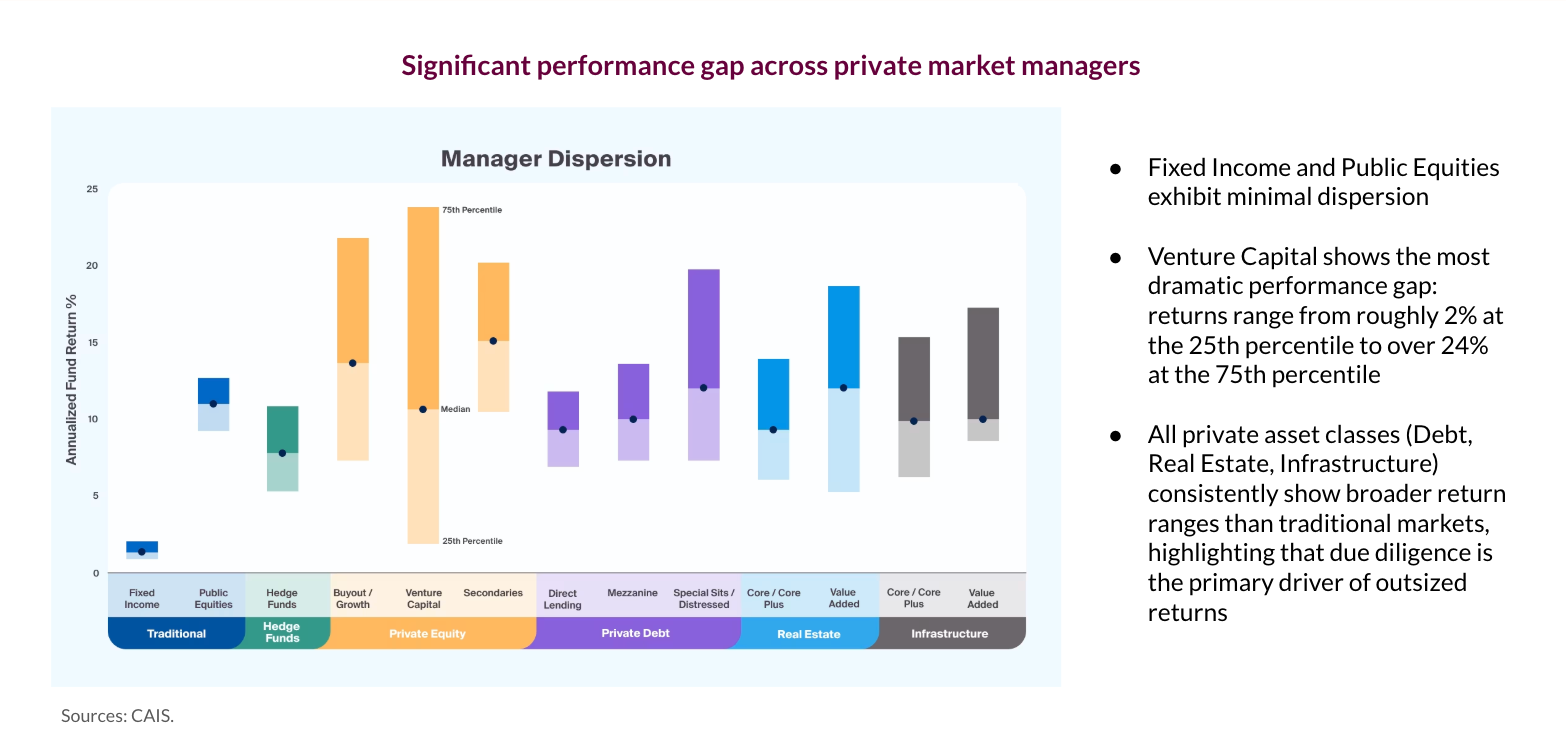

4. Manager selection drives outcomes

Performance dispersion in private markets is materially wider than in public markets.

In public markets, performance differences between managers tend to be relatively narrow. In private markets, the gap between top and bottom quartile funds can be wide. That dispersion shifts attention from broad market exposure to manager selection.

A fund that lands near the median may deliver returns comparable to public benchmarks while still requiring a long-term capital commitment. Illiquidity alone does not create excess return. The source of performance matters.

Understanding how value is created inside a fund is central to underwriting the opportunity. Return attribution analysis can clarify whether performance stems from revenue growth and margin expansion or from leverage and multiple expansion. Funds that rely heavily on financial engineering may present different risk characteristics than those built on operational improvement and disciplined execution.

The J-curve dynamic is also an important consideration. Early years may reflect muted or negative reported returns as capital is deployed and fees are paid, with distributions occurring later in the lifecycle. Patience and expectation-setting are part of responsible allocation.

Manager quality, sourcing discipline, alignment of incentives, and operational capability all play a significant role in shaping long-term outcomes. A manager’s track record, while not a guarantee of future results, is a good place to start when making an assessment.

5. Private markets require informed participation

Investing in private markets involves committing to structures, timelines and reporting dynamics that differ meaningfully from public securities. Capital is typically committed for extended periods, liquidity is limited and performance unfolds over a multi-year lifecycle rather than on a quarterly cadence.

A clear understanding of those characteristics supports more intentional allocation decisions. Defining the role private markets are intended to play within a portfolio provides useful context for evaluating strategies and sizing commitments. Objectives may include income generation, diversification, long-term capital appreciation or exposure to earlier-stage growth.

Liquidity planning and pacing warrant careful consideration. Private investments often involve gradual capital calls and distributions over time. Aligning commitments with broader financial objectives, time horizon, and risk tolerance remains central to disciplined portfolio construction.

Education underpins each of these decisions. Familiarity with fund structures, return drivers, risk factors and the interaction between private and public exposures supports more deliberate participation as the opportunity set continues to expand.

The future of private market investing

Private markets continue to expand in scale and complexity. Companies are remaining private longer, capital formation is occurring outside traditional channels, and the range of available strategies continues to grow.

As that landscape evolves, so does the need for clarity. Portfolio construction increasingly requires a deeper understanding of strategy design, manager selection, liquidity planning and how private exposures interact with public holdings. Education becomes a critical part of responsible participation.

At Alto, that commitment extends beyond a single series. We will continue prioritizing investor and advisor education, convening experienced practitioners, and partnering with teams like Long Angle to bring institutional insight into broader industry conversations. Our goal is to equip our community with the frameworks and context needed to navigate private markets thoughtfully as the opportunity set continues to mature.

The future of private market investing will be shaped not only by access, but by understanding.